Health Insurance Awareness in India and its Problems

- 15 June 2022

- Click to Read...

India is home to approx. 1.39 bn people. Some might argue that spreading awareness about health insurance is an easy task given the strong manpower. However, this is one of the biggest challenges of why health insurance penetration is low in India. We have strict rules about buying a motor insurance policy, but health insurance is not compulsory even though it ensures timely medical treatment. Let's deep dive into the issues related to health insurance awareness in India, through this article.

Importance of health insurance awareness Lack of health insurance awareness leads to people paying for the cost of medical treatment themselves. While this seems like a normal thing, it can become a serious issue if the medical bill burns a hole in your pocket. This issue is topped by the increasing costs of medical treatments. Getting treatment for a simple medical procedure may need thousands of rupees if performed in a private hospital. Choosing the right health insurance plan can combat this issue. People can enroll under government health schemes like Arogya Sanjeevani to get holistic coverage at affordable premiums.

What are the major difficulties in spreading health insurance awareness?

Apart from a large population and lack of reach, the following are the major challenges to health insurance awareness in India.

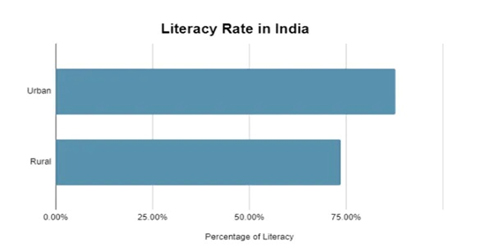

Illiteracy According to a report from the Ministry of Statistics & Programme Implementation, the literacy rate in India stands at 77.7% in the year 2020-21. A significant part of the Indian population is still illiterate. Additional efforts must be made to specially design awareness programs for people who are not sufficiently educated. They need to be made aware that health insurance can help mitigate financial issues while availing of health care facilities.

As the chart indicates, the illiteracy issue is not limited to the rural areas but is present in the urban sections also. Thus, illiteracy and lack of awareness about health insurance are issues faced by people in cities as well.

Deep-rooted misconceptions about health insurance One of the most common misconceptions about buying health insurance is that healthy people don’t need it. The seriousness is felt only while facing a medical contingency. However, by this time, the waiting period clause of the insurance plan activates and thus fuels another major misconception related to claim rejection. People believe that health insurance companies reject most claims. But in reality, health insurance claims are accepted when they are raised as per the terms and conditions of the policy.

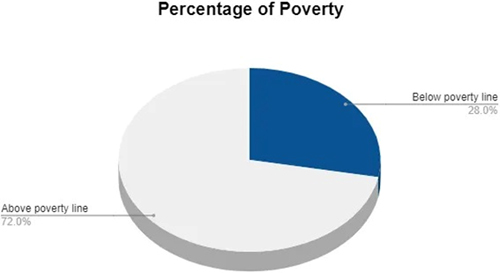

Poverty As per the United Nation's report, India is estimated to have nearly 364 million people that fall below the poverty line. This is nearly 28% of the Indian population. This section of society fights more pressing issues like lack of food and sanitation. Thus, spending money on health insurance is probably not on their priority list.

Free health insurance programs along with good medical facilities will be helpful. These will be useful in increasing awareness and improving health insurance penetration in the country.

The state of public hospitals Public hospitals are the prime location where health insurance awareness can be magnified. However, the lack of basic facilities has led people to rely more on private hospitals in spite of higher costs. Public hospitals are also dependent on government funds to operate, but these funds prove to be insufficient. On the other hand, medical technology is changing rapidly but is fuelled by high costs. Thus, public hospitals lag and cannot offer the latest medical treatment available in private hospitals. State-run health insurance awareness programs can help in educating the masses about its importance. Public hospitals must tie up with health insurance companies on a local level to ensure better reach in places that lack medical facilities.

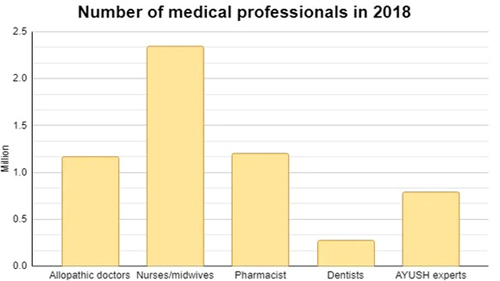

Lack of healthcare professionals Healthcare workers play a pivotal role in spreading awareness about proper health care and possibly the importance of health insurance. If an adequate number of people are available to provide medical facilities, then these professionals can contribute towards educating patients as well.

As per the Economic Survey 2019-20, India has a doctor-to-patient ratio of 1:1456. Whereas 1:1000 is the ideal ratio as per WHO. The rippling effect of the low number of healthcare professionals was evident during the COVID-19 pandemic.

Free coverage under Group Plans Employee-centric organizations offer free health insurance plans to cater to their employee’s medical needs. Many people depend on this coverage and refrain from buying a comprehensive policy that offers flexibility and personalized coverage. Employees can thus become adamant to get coverage only under such corporate plans and may turn a blind eye to government health schemes. However, a corporate plan does not offer lifetime validity. The policy ends upon the end of employment which leaves the ex-employee and the dependants exposed to medical liabilities.

A Possible Solution Spreading awareness about health insurance is similar to taking part in a relay race. Each team member is of equal importance here. The government, healthcare professionals, health insurance companies, and eventually the population can form the pillars of spreading awareness to the deepest parts of the country. Remember that a suitable health insurance policy will be the ultimate support in case of a medical emergency. Nowadays, health insurance is not limited to hospitalization but includes many other services as well. Thus, buying a policy with adequate coverage and useful services from a reliable insurance company can make things go smoothly during a medical emergency.

How Does Life Insurance Work?

- 08 June 2022

- Click to Read...

Life insurance is a contract between you and an insurance company. Essentially, in exchange for your premium payments, the insurance company will pay a lump sum known as a death benefit to your beneficiaries after your death. Your beneficiaries can use the money for whatever purpose they choose. Often this includes paying everyday bills, paying a mortgage, or putting a child through college. Having the safety net of life insurance can ensure that your family can stay in their home and pay for the things that you planned for. There are two primary types of life insurance: term and permanent life. The permanent life insurance such as whole life insurance or universal life insurance can provide lifetime coverage, while term life insurance provides protection for a certain period.

What Does Life Insurance Cover?

Life insurance covers all causes of death, with one main exception: Suicide within the first two years of owning the policy. Apart from that exclusion, life insurance covers death from illness, disease, accidents, and homicide. Regardless of the cause of death, a life insurance company could deny a claim if it believes there was misrepresentation on the life insurance application, especially if the death is within the first couple of years of owning the policy. For example, if someone lies about their health or other information on the application, the life insurance company could deny a claim by the beneficiaries. In other extremely narrow cases, a life insurance claim could be denied if the beneficiary killed the insured person, or if the claim is disputed by someone who says the policyholder was coerced into changing the beneficiary.

Main Types of Life Insurance

Term Life Insurance In addition to being the most affordable type of life insurance, term life insurance is the most popular type of life insurance sold (71% of purchasers) according to the Insurance Barometer Report.

Term life insurance provides coverage for a certain amount of time and the premium payments stay the same amount for the duration of the policy. Typical choices are policy lengths are 10, 15, 20, 25, or 30 years.

If you pass away within the term of your policy, your beneficiaries can make a claim and receive the death benefit money, tax-free. Once the term of the policy expires, you may be able to renew the coverage in increments of one year, known as guaranteed renewability. But each year of renewal will be at a higher rate.

Permanent life insurance Permanent life insurance provides lifelong coverage. It’s more expensive than term life because of it:

- Can last for the duration of your life.

- Usually builds cash value.

The cash value component accumulates on a tax-deferred basis over the life of the policy. It acts as a savings portion of the policy. Typically, you can borrow against the policy’s cash value or make a withdrawal. If you decide to end the policy, you can get the cash value minus any surrender charge. In some policies the cash value may build slowly over many years, so don’t count on having access to a lot of cash value right away. Your policy illustration will show the projected cash value.

There are several varieties of permanent life insurance:

- Whole life insurance offers a fixed death benefit and a cash value component that grows at a guaranteed rate of return. Many whole life insurance policies pay out dividends that can be used to reduce premium payments or can add to your cash value.

- Universal life insurance often offers more flexibility than a whole life insurance policy. You may be able to alter your premium payments and death benefit, within certain limits. With a universal life insurance policy, the cash value will build depending on the policy type. For example, an indexed universal life insurance policy will have cash value tied to an index such as the S&P 500. A variable universal life policy will typically have investment subaccounts that you can choose and manage.

- Burial insurance is a small whole-life policy with a small death benefit, often between $5,000 and $25,000. Burial insurance is designed to cover only funeral costs and final expenses.

- Survivorship life insurance or “second to die life insurance” insures two people under one policy, usually a married couple. When both spouses have passed away, the policy pays out the death benefit to the beneficiaries. Usually, survivorship life insurance is part of a larger financial plan to fund a trust or pay federal estate taxes.

How to Choose the Right Life Insurance Policy Type

With all of the life insurance options available, it may seem complicated to choose the right one. Start by deciding between term life and permanent life insurance. Consider a term life insurance policy if you need life insurance for a specific amount of time. For instance, if you want insurance to cover your working years as possible “income replacement” if you were no longer around. Term life insurance is also a good choice if your budget is limited. Since term life insurance provides protection for a specific amount of time, and it’s not a cash value life insurance policy, the rates will be lower than permanent life insurance.

As you enter different stages of life, your life insurance needs may change. Many term life insurance policies are convertible to a permanent policy. The options will depend on your policy and insurer. Term life conversion allows you to switch to a permanent policy without re-applying or taking a life insurance medical exam. On the other hand, a permanent life insurance policy will last for the duration of your life. If building cash value is important to you, look at permanent life insurance options.

But if you’re purchasing a permanent policy only to capitalize on the cash value accumulation, depending on the policy, you’re better off putting your money into a savings or investment vehicle, so you’re not paying for the life insurance and charges within a permanent policy. And cash value isn’t typically intended for beneficiaries. Upon death, any cash value generally reverts back to the life insurance company. Your beneficiaries get the policy’s death benefit, not the death benefit plus cash value.

That said, some policy types will offer the death benefit plus cash value, but for a higher price.

How Much Does Life Insurance Cost?

The cost of life insurance varies significantly depending on several different factors. One of the biggest cost factors will be the type of life insurance you buy. For example, a term life insurance policy is significantly less expensive than a whole life insurance policy for the same amount of coverage.

Here are some of the most common factors affecting life insurance rates:

- Age. The younger you are when you buy a policy the less, you’ll pay. That’s because your chance of death is smaller.

- Sex. Females have a life expectancy that is nearly five years longer than males, according to the National Centre for Health Statistics. This means that men generally pay more for life insurance than women (except in Montana where insurers must provide gender-neutral life insurance rates).

- Health. Your health has a major impact on your life insurance rates. The insurer will evaluate your past and current medical conditions in order to calculate your life expectancy.

- Lifestyle. Your driving history (such as a DUI conviction), criminal record, and dangerous occupations and hobbies (such as scuba diving) can all result in higher life insurance rates.

How to Choose a Life Insurance Coverage Amount

A good rule of thumb for estimating how much coverage you need is to:

- Add up all the expenses you want to cover, such as income replacement for your work, a mortgage, and children’s college expenses.

- From that, subtract the amounts that your family could use to cover those expenses, such as savings and existing life insurance. Leave out retirement savings if your spouse will need that later.

The resulting number is how much life insurance you need. It may look high, especially if you’ve factored in income replacement for many years. Still, life insurance quotes are free, so it doesn’t hurt to price out the coverage you need. If it turns out to be unaffordable, you can buy what you can afford now to lock in a good rate. You can buy more later, just be aware that several years from now your rate will be based on your older age and any health conditions you’ve developed.

How to avoid falling prey to mis-selling of insurance policies

- 01 June 2022

- Click to Read...

With the spread of the pandemic, more and more people have started opting for insurance, mostly health and life insurance. In India, quite a large number of insurance products are sold through brokers and agents. Even though some brokers and insurance agents may be well-intentioned, most are seen making fake promises to policyholders to get their way. Mostly, buyers with limited knowledge about insurance products, look up to these agents hoping to get help while choosing policies that are suitable for their needs and lifestyle.

However, it’s often seen that some rogue agents take advantage of such buyers and misrepresent facts or even give a distorted picture of the features of the policy while selling an insurance policy. Hence, experts suggest buyers should be aware of such agents and the ways in which insurance can be mis-sold to them while buying a policy. Even without being misled by agents, there are ways through which policyholders have been misled and mis-sold insurance policies. Hence, policyholders should always ask questions, carefully read the proposal and final documents of the policy and beware of fake promises made before signing off.

Here are some of the common ways of miss-selling policies to customers:

- It’s a red sign if the policy benefits are not explained clearly to you. Agents have to explain the policy benefits and features accurately to the buyer. Hence, if you are still unclear about them, and the agent has not explained to you the policy features and benefits properly, and refuses to explain further, know that there is something wrong. Keep in mind that you will be paying the premium for getting benefits, which should be explained in advance.

- There are agents who exaggerate, distort, and also state false promises to make their policy show attractive rates of returns to the buyer. Hence, experts say customers be aware of such fake promises.

- Some brokers and insurance agents promise that insurance plans give better returns than bank fixed deposits and some other investment avenues. If you’re told similar things, then know that it may not be true. Industry experts say promising insurance plans giving better returns than bank FDs is one of the most common ways of selling insurance. Hence, do not fall for statements like – an insurance policy is a safer option and gives better returns than an FD. Also, keep in mind that insurance policies and savings/investments are entirely different instruments. They should not be mixed or compared.

- Another point where many buyers are mis-sold policies is premium payment. Agents not only exaggerate the benefits of the policy but also give misleading information on premiums. While buying a policy, commit to a premium amount that will be easily payable by you. Till the time a policyholder pays their premiums on time and for the full term of the policy, any insurer is liable to honour its side of promises made in the product. But if the policyholder has not paid the premium for the full term, the claim process changes. The insurers could also charge additional charges.

- The claim procedure has mostly to do with the health and accident insurance policies. Policyholders need to know from their agents while buying a policy, exactly under what all circumstances can the policyholder make a claim, what type of claim is payable, and what is not. While mis-selling agents give the impression to the policyholders that anything and everything is covered under an insurance policy, which is not true. All insurance policies have exceptions. Hence, it is better to find out under what circumstances or conditions will the claim not be payable

How to revive a lapsed policy

- 25 May 2022

- Click to Read...

An insurance policy lapses when you stop paying the premiums on the due date and during the 30 days of the grace period. Depending on the nature of the policy, it could either lapse automatically or allow a window for revival. Typically, insurers are required to offer a revival period of two years for policyholders to reinstate their policies

Pure risk covers: In case of pure risk covers like term plans, the policy lapses if you don’t pay the premium even during the grace period. You may have to let go of the premiums as well as the assured benefit.

Unit-linked insurance plans (Ulips): In the case of Ulips, you can revive the policy up to two years from the date you first missed paying the premium. If you skip paying the premium in the first five years or during the lock-in period, the policy is considered lapsed after a 90-day period and the insurer moves the fund value to the discontinuance fund and levies a discontinuance charge (a maximum of ₹6,000 if discontinued in the first year). If you skip paying the premiums after the lock-in period, the insurer will give you an option to revive the policy.

Traditional plans: If you don’t pay the premium for traditional plans before they acquire a surrender value (paid-up), then you may lose all the premiums paid. But if the policy becomes paid-up, it doesn’t lapse and continues with a reduced sum assured. Traditional policies acquire surrender value after two to three annual premiums are paid.

If it’s been more than two to three years since your policy lapsed, the only time you can revive it is if your insurance company comes up with special campaigns like the one LIC has launched currently.

How to spot and deal with fake insurance agents

- 05 May 2022

- Click to Read...

A few newspapers, DNA for instance, carried an advertisement by Life Insurance Corporation (LIC) of India yesterday (see here), warning customers against fake calls from unauthorized people pretending as LIC agents. The ad cautioned against getting cheated by such impersonators. To know more read on.

How this works: There are several ways these fraudsters work, here are a few examples.

For instance, if you are an existing LIC policyholder, the fraudster gives you a call, and advice you to stop paying premiums towards your existing policy since it's lapsed due to some reason, or they ask you to surrender your policy. They might further tell you; new policies are being offered to you by the insurers with better terms, and you no longer need to continue with the existing policy. "They lie that a new policy needs to be issued and since with the new policy they get a mouth-watering commission in the first year itself”.

Another tactic is that they pretend to be LIC employees and promise huge bonuses and elevated returns when you buy a policy for them.

At times, this fraud goes beyond promising false bonus amounts to entice you to buy a policy. Here, the agents sell you policies for which you pay premiums. But the premiums are credited to the agent’s account and the agent gives you fake receipts which look like authentic receipts. While you think your money is invested in a policy, the agents are ripping you off your money.

According to this report published in the Hindustan Times on May 12, 2102, a 71-year-old widow from Delhi was coined by a fake agent, who said he was from LIC. In fact, not only LIC's name but fraudsters are also posing as representatives of the watchdog Insurance Regulatory and Development Authority (IRDA). Take, for instance, this complaint filed at the Indian Consumer Complaint Forum. Here the victim received a call from a fraudster who posed to be an agent from IRDA. He told the victim that he was entitled to a bonus for a life insurance policy he had with an insurance company. But to realize the cheque, the victim would have to make an investment first.

WHAT TO DO?

If you get a call from someone claiming an IRDA agent, you can be sure that the caller is a fake agent or fraudster for the simple reason that the regulator does not make such calls. "The general public is hereby informed that the Insurance Regulatory and Development Authority is a regulatory body which does not involve directly or through any representative in the sale of any kind of insurance or financial products," a public notice posted on its website said. It further adds that if you make any kind of transaction with such a fake agent, you would be doing so at your own risk. Likewise, if you receive calls from an agent claiming LIC or any other insurance company for that matter, it's best to disconnect the call.

Instead, you should call the insurer's call center number mentioned on their website, to get more details. Also keep in mind that if any agent asks you to pay cash, it should be an immediate red flag. According to the LIC's advertisement, when you buy a LIC policy, you should register the same on their portal for easier management of the policy. Also, when agents visit you, you should check their license, issued by LIC. But then, we think it isn't too difficult for fraudsters to make fake licenses. So, may be paying a visit to the insurer’s branch office or buying a policy online via the company's website or online insurance portal, would work better.

Is Mental Illness Covered under Health Insurance?

- 20 Apr 2022

- Click to Read...

Mental illness is something that is considered to be taboo. It is a topic that society does not want to talk about and has pushed behind closed doors. But now, the thinking of people is changing. Young people prefer to disclose than hide. They prefer to be cured than be left in a trap.

Here, the Insurance Regulatory and Development Authority of India (IRDAI) has come up to help bring the change.

Recently, IRDAI issued a circular directing all insurance companies (except ECGC and AIC) to comply with the provision of the Mental Healthcare Act, 2017 before 31 October 2022. According to the Mental Health Care Act, of 2017, all insurance companies need to provide coverage for mental illness under health insurance policies on the same basis as given for physical illness. This Act came into force in May 2018.

IRDAI said, “All insurance products shall cover mental illness and comply with the provisions of the MHC Act, 2017 without any deviation. Insurers are requested to confirm compliance before October 31, 2022.” An important point to be noted is that this may not cover existing mental illness or illness by birth. One needs to declare all facts with honesty and let the insurance company decide about acceptance or rejection.

Does Health Insurance Cover Mental Illness?

Earlier, health insurance did not cover mental illness. But people are more open to talking about their mental health or well-being. In 2018, IRDAI made it mandatory for all insurers to cover mental illness under health insurance. And now IRDAI has again asked them to confirm compliance by this October 31.

What are the Inclusions of Mental Health Insurance?

A mental health insurance plan is similar to a normal health insurance plan that covers physical illness. It covers-

- In-patient hospitalization expenses including

- Cost of Treatment

- Room Rent

- Medicine Expenses

- Ambulance Charges etc.

- Some insurers offer OPD benefits too. These insurers will cover the cost of consultation, counselling as well as rehabilitation for mental diseases.

- Mental diseases covered:

- Schizophrenia

- Obsessive-compulsive disorder (OCD)

- Anxiety disorder

- Bipolar disorder

- Acute depression

- Dementia

- Psychotic disorder

- Attention deficit

- Mood disorder, etc.

How to Stay Protected Against Insurance Frauds?

- 02 Apr 2022

- Click to Read...

This year the International Fraud Awareness Week is from November 13 to 19. A week that focuses on fraud detection and prevention. We are in the middle of a global crisis and trying our level best to adapt to the new normal. Internet banking penetration has increased since the outbreak of COVID-19. This somewhere has also led to incidences and attempts at digital fraud. Hence, it becomes important to take steps that minimize the impact of fraud. Moreover, promote anti-fraud awareness and education. Fraud Awareness Week is an apt time to take a step further and be an anti-fraud professional.

What Can You Do?

It is important to be aware of what's happening. When you are aware, you are a more conscious person and can easily have productive conversations. It helps to figure out if anything goes wrong. Have conversations around fraud prevention. It could be with your peers, co-workers, family members, and so forth. Fraud prevention is important for society as a whole. In this article let us discuss insurance fraud.

How Does Fraud Affect?

Fraud not only affect the common people but also the insurance industry. Since the commencement of insurance as a commercial enterprise, insurance fraud has existed. It takes different forms and can occur in any insurance domain. Insurance fraud could be either soft or hard.

Difference Between Soft Fraud and Hard Fraud

Soft frauds are more common, and it includes exaggeration of the legitimate claims by the policyholders. Sometimes it is also referred to as opportunistic fraud. But when anyone deliberately plans a loss, such as setting fire to property or theft of a motor vehicle that is covered under the insurance policy. This is referred to as hard fraud. Amidst COVID-19, insurance frauds have been on a rise. It is imperative to protect yourself from the fake insurance policies available in the market. An unaware customer is usually targeted by fraudsters. The simple way of fleecing the customers is by offering cost-effective insurance premium rates. Well, you might think that insurance fraud is not something new. However, there has been a significant rise in such scams. Particularly in the segments of health insurance, motor insurance, and personal accident. Some fraudsters file cases of natural deaths as a victim of road accidents to claim money from the personal accident insurance policy. To counter any such insurance fraud, preventive measures need to be taken by both the insurance company and the insurer.

How to Check Whether the Insurance Policy is Fake or Not?

To help you check whether the insurance policy is fake or not, listed below are some key tips:

Buy Policies from Licensed Insurers Whether you plan to buy motor insurance or medical insurance the purchase will be either done offline or online. In case you are making an offline purchase, ensure that the agent has a license. Look for the ID card and click a picture of it from your mobile phone. In case you are buying an insurance policy online, check the credentials of the website. If required, read the customer reviews and go with a company that has a good claim settlement and solvency ratio.

Receipt of Premium Payment It is recommended to pay the insurance policy premium online. Or through a demand draft/cheque in the name of the insurance company. Ensure that you keep the premium payment receipts safe for future reference. If possible, look for an option whether you could have a copy of the proposal form that can be reviewed later.

Use the QR Code IRDAI has made it a mandate for all the motor insurance policies issued on or after 01 December 2015 onwards to have a QR code. So, while buying motor insurance scan the Quick Response code to check the authenticity of the policy purchased. With a QR code in place, other relevant details about the policy can also be found easily. In case of any dilemma or query, you can also speak to the customer support of the insurance company.

Do Not Sign a Form Without Reading It Regardless of whether you are buying the insurance or filing a claim do not sign a blank paper. Do not sign a form without reading it. Fill in the information yourself and provide the correct information. It is good to remain #Bimasavdhaan

Over to You Let us try not to be a victim of insurance fraud. In case you are not aware of something try to gather information about it. Perpetrators always have their ways of subverting the system. Take your time, stay alert, and be cautious of insurance scams. Do not fall prey to any spurious calls in the name of any government authority. If you find anything to be suspicious, contact the nearby police station. Also, get in touch with the insurance company. On good or rough days, paying heed is always going to be a virtue. Let us make efforts to minimize the impact of fraud by preventing, recognizing, reporting, and stopping it.

Anti-Money Laundering Guidelines (AML) Guidelines

- 15 Mar 2022

- Click to Read...

AML Guidelines refer to Anti-Money Laundering Guidelines, which are a set of guidelines and best practices designed to prevent and detect money laundering and terrorist financing. The guidelines are typically issued by regulatory bodies or industry associations to help financial institutions comply with AML laws and regulations.

The key features of AML Guidelines include:

Customer Due Diligence (CDD): AML Guidelines require financial institutions to perform CDD procedures to identify and verify the identity of their customers. This includes obtaining information such as name, address, and other identifying information.

Suspicious Activity Monitoring and Reporting: Financial institutions are required to monitor customer transactions for suspicious activity and report any suspicious transactions to the relevant authorities.

Record Keeping: Financial institutions are required to maintain accurate and complete records of customer transactions and AML compliance efforts.

Risk Assessment: AML Guidelines require financial institutions to assess and mitigate the risks of money laundering and terrorist financing.

Training: Financial institutions are required to provide regular AML training to their employees to ensure that they are aware of the latest AML regulations and best practices.

Overall, AML Guidelines are important for financial institutions to prevent and detect money laundering and terrorist financing. Compliance with AML Guidelines is necessary for financial institutions to avoid legal and reputational risks and to promote the integrity of the financial system.

Claim repudiation on the grounds of concealment

- 12 Mar 2022

- Click to Read...

Claim repudiation on the grounds of concealment of fact is a common practice in the insurance industry. When a policyholder applies for insurance, they are required to disclose all material facts related to their health, occupation, income, lifestyle, and any past claims history.

Material facts are those that could influence the insurance company's decision to provide coverage or affect the premium amount. If a policyholder conceals or misrepresents any material fact while applying for insurance, the insurance company has the right to reject the claim in case of a mishap. This is known as claim repudiation on the grounds of concealment of fact. For example, if a person applies for life insurance and does not disclose their smoking habit, and then dies due to lung cancer, the insurance company can repudiate the claim on the grounds of concealment of fact. Similarly, if a person does not disclose their pre-existing medical condition while applying for health insurance, the claim for treatment related to that condition can be rejected.

However, claim repudiation on the grounds of concealment of fact is subject to certain conditions. The insurance company must prove that the policyholder intentionally concealed or misrepresented the material fact and that it was directly related to the mishap. If the insurance company cannot prove these conditions, the claim cannot be repudiated.

Therefore, it is important for policyholders to disclose all material facts accurately while applying for insurance to avoid claim repudiation. Insurance companies must also carry out thorough background checks and use technology to detect any fraudulent activity to maintain the integrity of the insurance industry.

The IRDAI Fill and Use Guidelines

- 01 Mar 2022

- Click to Read...

The IRDAI Fill and Use Guidelines are a set of guidelines issued by the Insurance Regulatory and Development Authority of India (IRDAI) that provide guidance on the design, pricing, and underwriting of insurance products. The guidelines aim to ensure that insurance products are fair, transparent, and provide adequate protection to policyholders. The key features of the IRDAI Fill and Use Guidelines include: Product design: The guidelines prescribe the principles and guidelines for product design.

They require insurance companies to ensure that the products are fair, transparent, and provide adequate protection to policyholders. Pricing: The guidelines prescribe the principles and guidelines for pricing of insurance products. They require insurance companies to ensure that the pricing of the products is fair, reasonable, and based on sound actuarial principles. Underwriting: The guidelines prescribe the principles and guidelines for underwriting of insurance products.

They require insurance companies to ensure that the underwriting process is fair, transparent, and based on sound actuarial principles. Policy documentation: The guidelines prescribe the principles and guidelines for policy documentation. They require insurance companies to ensure that the policy documents are clear, concise, and written in plain language. Disclosure requirements:

The guidelines prescribe the disclosure requirements for insurance products. They require insurance companies to disclose all material information related to the product, such as the benefits, exclusions, and limitations. Overall, the IRDAI Fill and Use Guidelines are aimed at ensuring that insurance products are designed, priced, and underwritten in a fair and transparent manner. The guidelines seek to protect the interests of policyholders and promote a healthy and vibrant insurance sector in India.

How to avoid rejection of insurance claim

- 28 Feb 2022

- Click to Read...

In a world of uncertainties, term insurance provides a safety net for families suffering in the unfortunate event of the demise of their breadwinner. But have you ever wondered what will happen if your term insurance claim gets rejected due to some reason?

One can shudder at the thought of rejected term insurance. This is because, after the death of the policyholder, their family is left in a state of shock, if it was assumed that the money would flow in, otherwise not. The loss of their earner cuts deep into their financial position. Such an incident leaves the family clueless and in dire need of stability and financial security.

To avoid adding misery to an already unfavorable time, it is essential to know what may lead to a claim being rejected. lack of transparency While filling in your information for a term insurance policy, it is extremely important to honestly disclose all the required information to the insurers. This is important because a term-insurance policy is a means of securing your family’s future, and helps your insurer better protect you. By hiding important facts from the insurance company, people only give a bigger reason for rejection. However, this situation can be avoided by ensuring that you provide accurate and correct information regarding factors such as age, occupation, income, and existing policy details.

While selecting a new policy it is necessary to provide details about the pre-existing conditions as these details come up sooner or later anyway. unknown option Hence, it is best to be clear about such situations while signing up for the policy. This not only strengthens your case but also helps your insurer to process your request without any disruption. An insured’s lifestyle choices directly affect how much premium they will pay for their life insurance. These include unhealthy eating or other lifestyle choices such as smoking, drinking alcohol, and the like.

Data from the World Health Organization shows that India is home to 12% of the world’s smokers, with tobacco-related diseases killing more than 1 million people annually. Insurers offering term life insurance approve the policy and fix the premium amount based on various lifestyle and health factors. Such habits must be informed to the insurer while applying for term insurance. Also, people with hazardous hobbies like paragliding and deep-sea diving need to mention this to their insurers while applying for a term plan.

Doing so will help the insurance company to better assess your case and determine the best premium amount for you. handing over paperwork There are two parts to taking a term plan. The first involves research to find a suitable plan. The second part requires careful study of the documents and an understanding the terms and conditions of the policy. Usually, by the time people finalize the policy after thorough research, they are too tired to know about any more details. So they hand over the paperwork to the agents.

However, it is not advisable to entrust the responsibility of filling and submitting the insurance form to a third person. Since the financial future of our loved ones directly depends on it, it is our responsibility to be careful in these matters. Missing any important details in these forms and documents such as family medical history can cause problems later. pre-existing policies It is a common mistake for people to ignore the policy declaration rule which dictates that they should disclose their existing policies to the new insurer.

Many buyers are not aware of this. Be sure to inform your insurer about your sum insured, no matter how small or large. Failing to do so will definitely result in your claim being rejected. During the claims process, the column containing your medical history is taken into consideration. This is very important as it is directly related to your overall health graph and has a huge impact on the acceptance or rejection of your claim. As an important part of the proposal form, this section covers the medical conditions of the proposer and their family.

This is what helps the insurer to decide the amount of premium and whether the policy can be issued or not. nature of profession While people from all walks of life can opt for a term insurance policy, some occupations carry a high risk that is on the threshold of ‘life threatening’. People with jobs that require mine work and firefighters are part of this category. It is best to mention the nature of such jobs to your insurer to avoid further problems. At the time of claim, if an insurer believes that such information was hidden from them at the time of sign up, the claim may be rejected. A policy terminates when it loses its validity on paper – either because the term has expired or because premiums were not paid within the time limit. Filing a claim for a lapsed policy is a meaningless exercise that will get you nothing. In other words, any claim raised by you with the lapsed policy will be rejected.

Due date is important

Periodic premiums are required to be paid on or before the due date to maintain the validity of your term plan. However, if a policyholder fails to pay the premium on time, insurance companies provide a grace period of a few days. But it should be remembered that no claim will be paid if the policy is not renewed within the grace period. Therefore, it is necessary to take utmost care against policy lapses to protect against any untoward incident.

How to complain against an insurance company: Here are 6 ways

- 26 Feb 2022

- Click to Read...

There could be various reasons why an insurance policyholder might want to complain against an insurance company. Policyholders might want to raise a complaint related to the buying process, claim process, or generic service requests like changing addresses, contact details, nominations, offering tax saving certificates, payment method changes, and so on.

Register your complaint with the insurer A policyholder should first approach the insurance company itself to get their grievance addressed. You can approach the grievance redressal officer (GRO) of the insurance company. You can either visit the nearest branch or send an email to the GRO. While approaching the GRO you need to make sure that you give your complaint in writing along with the necessary supporting documents. You should not forget to take a written acknowledgment of your complaint with the date. Insurance companies have their own set of rules to manage customer complaints with all the relevant details like whom to contact and how to escalate the issue.

Wait for the insurer to resolve the issue As per IRDAI, the insurance company should ideally address your concern within 15 days. However, if your grievance is not resolved within 15 days, or if you are not satisfied with the resolution provided by the insurer you can escalate the issue to next level, i.e., you can take it to the insurance regulator, Insurance Regulatory and Development Authority of India (IRDAI).

Escalate it to IRDAI You can approach the Grievance Redressal Cell of the Consumer Affairs Department of IRDAI by calling the Toll-Free Number 155255 (or) 1800 4254 732 or by sending an e-mail to complaints@irdai.gov.in. Besides this, you also have the option to use the online portal managed by IRDA called Integrated Grievance Management System (IGMS). This is a way of escalating of your grievance so it should only be used after you have tried the grievance redressal channel of the insurance company. If you are not able to access the insurance company directly for any reason, IGMS provides a gateway to register complaints with insurance companies.

Make use of IRDAI's online portal IGMS: Many people often face a situation where the branch office of the insurer may not be willing to accept the written complaint and give an acknowledgment of the same. Or, the policyholder might face a problem in lodging his/her online complaint on the insurer's website. In such scenarios, it will be better to use IRDAI's IGMS facility. IGMS is a comprehensive solution that not only provides centralized and online access for the policyholder but complete access and control to IRDAI for monitoring market conduct issues of which policyholder grievances are the main indicators. IGMS classifies different complaint types based on pre-defined rules. It assigns, stores, and tracks unique complaint IDs. It also sends intimations to various stakeholders as required, within the workflow.

How to use IGMS

- Visit the website https://igms.irda.gov.in/

- Register yourself by entering your credentials

- Use Registered credentials to register complaints / view their status

It would be useful to keep the policy document ready while registering the complaint online. You can make optimum use of this system by giving accurate information about the complaint like the policy number, name of the insurer, complainant's contact details, etc. A complaint registered through IGMS will flow to the insurer's system as well as the IRDAI repository. Updating of status will be mirrored in the IRDAI system. In case the complaint is not fully attended to by the insurer within 15 days of lodging it, you may use the IGMS for escalating the complaint to IRDAI.

Send a letter to IRDAI with your complaint If you are unable to use the online methods, you can go for using the offline route. You can also download the IRDAI complaint from here and send your complaint through courier or post to the following address:

General Manager Consumer Affairs Department-

Grievance Redressal Cell,

Insurance Regulatory and Development Authority of India (IRDAI),

Sy. No.115/1, Financial District, Nanakramguda, Gachibowli, Hyderabad-500032

Raise the issue with Insurance Ombudsman If your complaint is still not addressed to your satisfaction, you can approach the appellate authority or the Insurance Ombudsman. The Insurance Ombudsman scheme was created by the government for individual policyholders to have their complaints settled out of the court system in a cost-effective, efficient, and impartial way.

There are at present 17 Insurance Ombudsmen in different locations across the country and any person who has a grievance against an insurer, may himself or through his legal heirs, nominee, or assignee, make a complaint in writing to the Insurance ombudsman within whose territorial jurisdiction the branch or office of the insurer complained against or the residential address or place of residence of the complainant is located.

There are certain conditions that you need to adhere to before approaching the Insurance ombudsman. As IRDA's consumer education website https://www.policyholder.gov.in/ you have to first approach your insurance company with the complaint. However, if they have rejected it or did not resolve it to your satisfaction or have not responded to it at all for 30 days then you may approach the Insurance ombudsmen. Moreover, your complaint should be related to a policy that you took in your individual capacity and the value of the claim including expenses claimed is not above Rs 30 lakh.

How the settlement process works with the ombudsman Settlement by recommendation: The Ombudsman will act as a mediator and will arrive at a fair recommendation based on the facts of the dispute. If you accept this as a full and final settlement, the Ombudsman will inform the company which should comply with the terms in 15 days.

Settlement by award: If a settlement by recommendation does not work, the Ombudsman will pass an award within 3 months of receiving all the requirements from the complainant and which will be binding on the insurance company. Once the award is passed, the insurer shall comply with the award within 30 days of the receipt of the award and intimate the compliance of the same to the Ombudsman.